How much can you save on your mortgage after RBA rate cut?

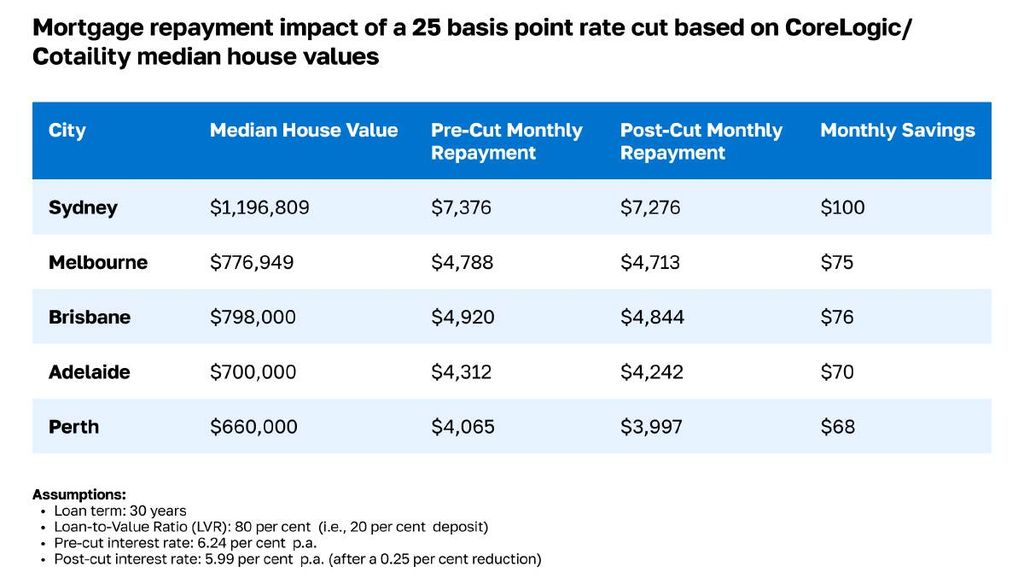

In a bold move not seen since the height of Covid-19, the Reserve Bank of Australia has delivered two rate cuts in three meetings, bringing the official cash rate down to 3.85 per cent.

The decision, anticipated by 88 per cent of experts in Finder’s RBA Cash Rate Survey, aims to ease mortgage stress and stimulate broader economic activity.

“Frankly, two cuts might not be enough to ease the spike in mortgage stress we’ve seen since rates started climbing again in May 2022,” Finder head of consumer research Graham Cooke said.

‘Maybe two more to go’

“But it’s a step in the right direction and great news for homeowners. It’s two down and maybe two more to go this year.”

If those additional cuts materialise, borrowers could save up to $5044 a year, assuming lenders pass on the reductions in full.

Cooke also noted the value of proactively shopping around:

You might like

“There’s a 40-point difference between the average and lowest rates available. You could effectively give yourself two rate cuts by refinancing.”

Chris Bates, CEO of Alcove Mortgage Brokers, said borrowers should take action now.

“There’s a refinance war brewing behind the scenes, with banks offering amazing pricing when you’re looking to leave,” he said.

“Don’t hesitate to reach out to your lender or a broker, they’re aggressively competing to retain customers.”

Changes to HECS, including a 25 per cent debt reduction and exclusion from mortgage assessments, combined with increased borrowing capacity (up around 2.5 per cent) are creating new opportunities for first-home buyers.

However, any newfound power may be offset by rapidly rising property prices.

Stay informed, daily

“There’s increased interest across the board since the first cut and the more that happens, the more it will build,” Bates said.

“However, upgraders are still very hesitant to take action under higher rates. If there are significant cuts with confidence that they will stay low, upgraders will come back strongly, as many families are not in the right property to suit their situation long term, and it makes sense to upgrade your home to a better tax-free growth asset.”

Demand expected to rise

“Buyers are still out and about, which is reflected in auction clearance rates consistently holding above 60 per cent,” LJ Hooker research head Mathew Tiller said.

“The decision by the RBA to reduce rates won’t shoot the lights out in the market by any means, as there are still affordability pressures due to recent price growth. But we anticipate seeing demand pick up as confidence returns. With more cuts expected, buyers will be looking to get in before rates fall further and demand strengthens.”

Yet broader economic risks are still in play, including international headwinds.

“The big unknown remains how Trump’s tariffs will impact Australia’s inflation rate,” said Nerida Conisbee, chief economist at Ray White.

“Supply chain disruptions and global pricing shifts could increase costs, though this might be offset by cheaper Chinese exports as they seek new markets. The RBA will be watching this closely.”

Conisbee said that while Australia’s property market had historically weathered global shocks (such as the global financial crisis and Covid-19) a repeat of the 2021 boom was unlikely.

“The market is strengthening, but we’re in a very different financial environment. During Covid, the cash rate hit 0.1 per cent and households were flush with savings. Today, the cost of living remains high, savings are lower, and rates won’t fall anywhere near those pandemic-era lows.”

She said that while price growth should continue, it would likely be more moderate and sustainable.

This article first appeared on View.com.au. Read the original here.

Want to see more stories from InDaily SA in your Google search results?

- Click here to set InDaily SA as a preferred source.

- Tick the box next to "InDaily SA". That's it.